Gift vs. Sponsored Projects and Distinctions from Other Forms of Funding

Defines sponsored projects, as distinguished from gifts, student aid and other supported activities and provides guidance related to making these distinctions.

Categories:

Recent Chapter Updates

-

Gift vs. Sponsored Projects and Distinctions from Other Forms of Funding

-

Gift vs. Sponsored Projects and Distinctions from Other Forms of Funding

-

Gift vs. Sponsored Projects and Distinctions from Other Forms of Funding

Questions about this policy?

Current Version: November 7, 2022

Original Version: June 21, 1979

1. Introduction

Both sponsored projects and gift-funded activities are externally-supported, with funds provided typically in response to a request or proposal. The classification of funding as "gift" or "sponsored project" will affect, among other things, the way Stanford University accounts for the funds, calculates and applies indirect (F&A) costs, and reports on the use of the funds to the sponsor or donor. For definitions of the various types of sponsored projects, see RPH: Categories of Sponsored Projects.

Administrative Staff involved in the processing of gifts, including cash, wire transfers or gifts of property, must complete Gift Administration at Stanford training.

Administrative Staff involved in sponsored research must complete Cardinal Curriculum Level I.

2. Definition of Sponsored Projects

Sponsored Projects are externally-funded activities in which a formal written agreement, i.e., a grant, contract, or cooperative agreement, is entered into by Stanford University and by the sponsor. A sponsored project may be thought of as a transaction in which there is a specified statement of work with a related, reciprocal transfer of something of value.

The following conditions characterize a sponsored project agreement, and help to distinguish such agreements from gifts.

A. Statement of Work

Sponsored projects are typically awarded to Stanford in response to a detailed statement of work and commitment to a specified project plan. As described below, this statement of work is usually supported by both a project schedule and a line-item budget, both of which are essential to financial accountability. The statement of work and budget are usually described in a written proposal submitted by Stanford University to the sponsor for competitive review.

B. Detailed Financial Accountability

The sponsored project agreement includes detailed financial accountability, typically including such conditions as:

- a line-item budget related to the project plan. The terms of the agreement may specify allowable or unallowable costs, requirements for prior approvals for particular expenditures, etc.

- a requirement to return any unexpended funds at the end of that period

- regular financial reporting and audit, including, for federal and state awards, accountability under the terms of OMB A-21, OMB-110 or the Uniform Guidance

A sponsored project budget will include the University's full negotiated indirect (F&A) cost rate unless a waiver of those costs has been approved. These conditions generally define the level of financial accountability associated with a sponsored project. While not all of the above conditions are necessary to define a sponsored project, they are collectively indicative of the increased level of financial accountability associated with such projects.

C. Disposition of Properties ("Deliverables")

Sponsored project agreements also usually include terms and conditions for the disposition of tangible properties (e.g., equipment, records, specified technical reports, theses, or dissertations) or intangible properties (e.g., rights in data, copyrights, and inventions). The presence of such terms and conditions in the agreement indicate that the activity is a sponsored project.

3. Definition of Gifts

A gift, on the other hand, is defined as any item of value given to the University by a donor who expects nothing significant of value in return, other than recognition and disposition of the gift in accordance with the donor's wishes. In general, the following characteristics describe a gift:

- A proposal/request may be submitted to the potential donor that includes a description of the proposed activities, with the understanding that the description of proposed activities is not intended as a commitment to a specific line of inquiry.

- Gifts may be accompanied by an agreement that restricts the use of the funds to a particular purpose. Beyond that, no contractual requirements are imposed (beyond the requirements of responsible stewardship) and there are no "deliverables" to the donor, e.g., no rights to tangible or intellectual property.

- There is no formal fiscal accountability to the donor beyond periodic progress reports and summary reports of expenditures. These reports may be thought of as requirements of stewardship, and, as such, may be required by the terms of a gift. They are not characterized as contractual obligations or "deliverables."

- Stanford agrees to use restricted gifts as the donor specifies, and does not accept gifts that it cannot use as the donor intends. If circumstances change such that a gift cannot be used as the donor specified, the donor must approve a change in the original restriction, or Stanford must receive court approval to waive the restriction (if the donor cannot be contacted). University approval for changes in the purpose of a gift fund can only be granted by the Provost.

4. Definitions of Fellowships, Scholarships and Other Student Aid

Fellowships are awards of financial support to individual named students or postdoctoral scholars, or to Stanford University on behalf of individual named students or postdoctoral scholars. At Stanford, fellowships funds are normally categorized as an award of “Student Aid”. However where the award of funding is made to Stanford University, where Stanford names the individuals to receive the support, and where the funds are to support research training, the funds are treated as a research training grant, a type of sponsored research project. See Attachment B. Checklist for Determining Whether Funding is a Postdoctoral Fellowship or a Sponsored Project below.

In order to facilitate the proper handling of fellowship support, the following procedures apply to proposal and award processes:

A. Undergraduate or Graduate Students (External Funding)

Students may apply for external fellowships in their own name. The process for submitting proposals will vary, depending on whether an institutional endorsement of the application is required by the funding source.

- Submissions requiring an institutional endorsement are submitted through the Office of Sponsored Research (OSR) or, in the School of Medicine, through the Research Management Group (RMG) Fellowship Office.

- Submissions which do not require an institutional endorsement may be submitted directly by the student.

Where funds are given to Stanford University to support named undergraduate or graduate students, those funds are received and processed through the Financial Aid Office, which administers the distribution of funds. Stanford University classifies these funds as “Student Aid.”

B. Postdoctoral Scholars

Postdoctoral Scholars who wish to apply for external fellowship funding must submit their application through either OSR or, in the School of Medicine, through RMG Fellowship Office. Awarded funds are received and processed by OSR, which administers the distribution of funds.

Postdoctoral Fellowships are not normally defined as sponsored projects. However, because they typically provide support for the recipient’s research activities, applications are processed through the research administration offices of the University. This process helps to assure appropriate internal controls as well as the inclusion of costs in the appropriate base for the calculations of Stanford’s indirect (F&A) cost rates and the appropriate classification of the research space.

5. Implementation and Administrative Issues

A. Guidance for Properly Distinguishing Gifts from Sponsored Projects

-

Distinctions Based on Source of Funds

Any funding provided by U.S. Government agencies, at the federal, state, or local level, in support of Stanford activities is a sponsored project. Government funds are not gifts.

-

Distinctions Based on Intent of Donor/Sponsor

In remaining cases, e.g., where funding is being provided by corporations, foundations or others not specified above, the distinction between gifts and sponsored projects will be made based on the proposal, statement of work, and terms of the agreement, taking into consideration the intent of the donor/sponsor.

In some situations, communication, including the proposal and award as well as conversations, makes it clear that the donor’s/ sponsor’s intent is to classify an award to Stanford as either a gift or a sponsored project. In these cases, the terms of the accompanying agreement may have to be adjusted in consultation with the donor/sponsor in order to clearly document the intent and avoid unintended classification.

B. Administrative Issues

1. Decision-Making in Unclear Situations

In some cases, the distinction between gift and grant, i.e., between a gift and a sponsored project, can be difficult to draw. Donors may sometimes use the word "grant" when the donation qualifies as a "gift" or vice versa. To ensure proper classification of gifts the Stanford Gift Transmittal system must be used.

If there are questions about the analysis or the user is unable to make a determination of gift or sponsored project, contact your Institutional Official in OSR or RMG.

Staff members from OSR, RMG or Corporate and Foundation Relations should consult as needed with the Associate Vice Provost for Research.

2. Donor/Sponsor Relations

In resolving issues related to the classification of an award, Stanford personnel must maintain an appropriate balance between the interests and preferences of the donor/sponsor and the University's administrative policies and objectives. In the process of resolving these issues it may be necessary to contact the donor/sponsor for clarification of intent and requirements, and/or to discuss the planned use of the funds.

If after consultation with the donor/sponsor there are still uncertainties about the donor/sponsor intent, a Conditions of Gift Letter should be used. Such contacts are usually best handled by the faculty member and/or development officer who initiated the activity.

3. Account Set-Up

Administrative Guide Memo 3.1.3: Activities/Accounts, specifies the procedure and responsibilities for establishing both sponsored project and gift accounts. Whenever a new account is requested, the responsible organization (Office of Sponsored Research in the case of sponsored projects, or Fund Accounting in the case of gift funding) verifies that the account (PTA) being set up is proper, in accordance with the definitions in this policy. These offices are responsible for assuring that a proper determination of gift or grant status has been made.

4. Indirect (Facilities & Administrative (F&A)) Cost Implications

Stanford's policy is to apply the University's full applicable indirect (F&A) cost rate to all sponsored projects. Gift funds will be assessed an infrastructure charge set by Stanford University, in accordance with the Infrastructure Charge Policy, Administrative Guide Memo 3.3.1. See in Related Items below RPH 15.2, Indirect Cost (F&A) Waivers for guidance relating to requesting waivers of indirect (F&A) costs. Indirect (F&A) costs are not charged on Fellowships, Scholarships or other student aid.

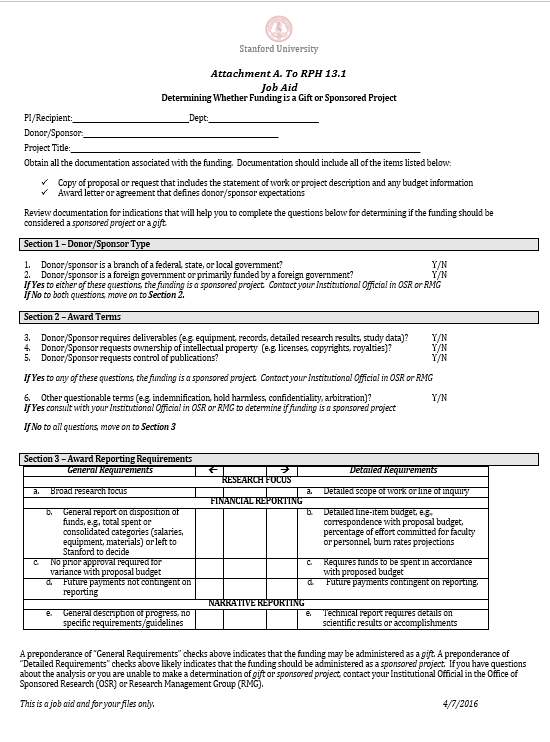

6. Attachment A. Job aid for Determining Whether Funding is a Gift or Support for a Sponsored Project

Attachment A. to this policy, the Job Aid for Determining Whether Funding is a Gift or Support for a Sponsored Project, reflects the on-line process through the Gift Transmittal System. This job aid is not intended to be used in routing a gift but only as a tool to help assist the user in the determination.

Within the Gift Transmittal System the user will be guided through a set of questions that reflect the job aid above. The answers will assist in the determination of whether the funding is in support of a sponsored project or gift. The transaction will then be routed for further review if necessary and subsequent processing.

If the answers reflect the characteristics of a gift, the transaction will be routed to and processed by Gift Processing as a gift.

If the answers show the user is uncertain, or that the gift reflects the characteristics of a sponsored project the transmittal is routed to either OSR or in the School of Medicine RMG for further review and a final determination. If the transaction is found to be a sponsored project the user will be notified via email.

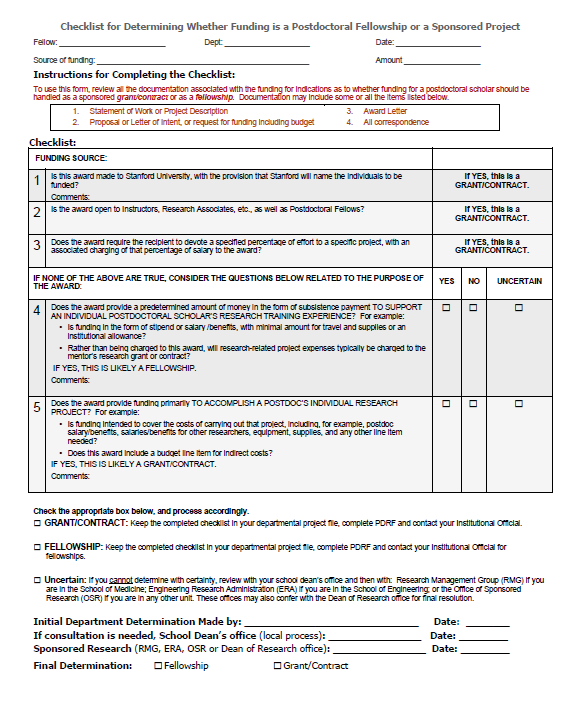

7. Attachment B. Checklist for Determining Whether Funding is a Postdoctoral Fellowship or a Sponsored Project

Attachment B. to this policy, Checklist for Determining Whether Funding is a Postdoctoral Fellowship or a Sponsored Project, can assist in making the determination as to whether funding should be classified as a Fellowship or Scholarship (i.e., student aid) or not.

8. Conditions of Gift Letter Templates

The Conditions of Gift Letter Templates are recommended for documenting simple, one-time expendable gifts from companies, professional foundations, and associations.

They clarify obligations and expectations such as:

- Intellectual property or data will be retained by Stanford

- Stanford's infrastructure fee will be applied

- Name use restrictions will apply

Request this Chapter’s Archives

Request permission to view & download archived chapters from the Research Policy Handbook.

Request Access to Research Policy Handbook Archive