Program Income

Defines Program Income and describes how to account for it.

Categories:

Recent Chapter Updates

Currently there are no updates available.

Questions about this policy?

Current Version: October 26, 2017

Original Version: October 26, 2017

1. Definition

Stanford defines program income as gross income earned by Stanford that is directly generated by a supported activity of a federal award or earned as a result of the federal award during the award’s period of performance.

2. What Is Included in Program Income

Program income includes but is not limited to income from:

- fees for services performed under the award

- the use or rental of real or personal property acquired under federal awards

- the sale of commodities or items fabricated under a federal award

- principal and interest on loans made with federal award funds

Registration fees collected under National Science Foundation supported conferences are considered program income.

3. What Is Not Included in Program Income

Program income does not include:

- license fees and royalties on patents and copyrights

- proceeds from the sale of real property, equipment or supplies

- interest earned on advances of federal funds

- rebates, credits, discounts, and interest earned on any of them unless specified in the award terms and conditions or regulations

4. Federal Contracts

If income is generated on a federal Contract contact the Director of Financial Compliance & Services (RFCS), listed above or the Office of Sponsored Research (OSR) for guidance.

5. Non-Federal and State of California Awards

Non-federal and State of California awards are not required to account for program income unless specified in the award terms and conditions or regulations.

6. Equipment

When using equipment acquired with funding from an active federal award to provide services for a fee contact the Director of RFCS.

7. Appendix A. Accounting Procedures for Program Income and Frequently Asked Questions

A. Accounting for Program Income on Federal Awards

There are three methods for use of program income from federal projects (i.e., awards, contracts or co-operative agreements) earned during the project period. Program income earned during the project period is retained by the Stanford and can be treated in one of three ways depending on policy, sponsor type, and/or terms and conditions of award:

- Additive: Program Income funds are added to available funds committed to the project by the sponsor, thus increasing the amount available to accomplish program objectives. The recipient must use the funds for the purposes and under the conditions of the award.

- Deductive: Total funds available to the project remain the same and the funds generated through Program Income are deducted from the financial commitment of the sponsor; and must be used to cover current costs of the project.

- Cost Sharing or Matching: Program Income is used to finance the non-federal share – cost sharing or matching requirements of the project

The additive method applies to research awards by default unless the awarding agency specifies another alternative. For non-research awards, the deductive method applies unless the awarding agency specifies to the contrary in its regulations or in the award.

B. Who do I Contact When Income is Anticipated or Generated from a Federal Award?

Department administrators should contact Research Administration Policy and Compliance (RAPC) or the Office of Sponsored Research (OSR) for guidance and directions if the PI plans to, or does, generate income from a Federal project. The rate of charging to use labs, services, materials, etc. is reviewed and approved by RAPC. In addition, the rates may need to be submitted to the government.

C. How do I set up a PTA for Program Income?

When program income is earned during the period of performance, a separate companion Oracle Program Income Award is set-up by OSR. To request a program income PTA initiate the OSR Request Form in the SeRA system. Program income is generated based on the support for the sponsored project and carries a 900 task number series. Departments should contact their post award representative in OSR for further assistance. Receipts and expenditures are recorded in the Program Income Award throughout the period of performance of the main award. Therefore, it is subject to the terms and conditions of the main award.

D. How do I Manage Program Income?

Billing is separated between internal vs. external customers.

1. Internal Customers

For internal customers, billing is done via journals. The Department Administrator who manages the Program Income award initiates an allocation journal to charge the benefiting PTAs and record revenue income to the Program Income PTA.

DR-58XXX-SPONSORED PTAs

CR-48110-PROGRAM INCOME PTA

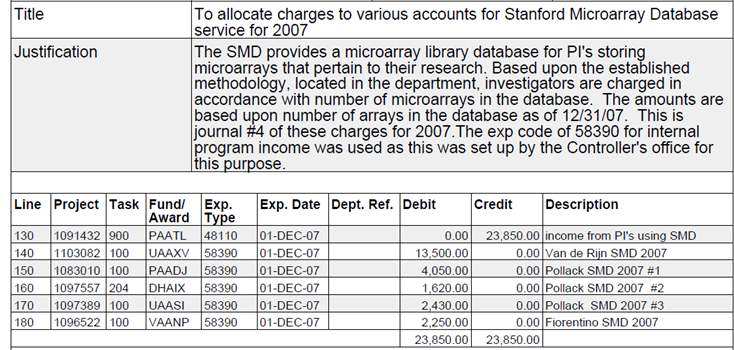

Sample iJournal

2. External Customers

For external customers, the Department Administrator who manages the Program Income PTA should contact Sponsored Receivables Management (SRM) in ORA for assistance with billing.

3. Revenue and Expense

Revenue

Department Administrators are responsible for recording the correct revenue object codes. There are only two options:

- Internal (48110 Interdept Revenue)

- External object code (46145 Other External Revenue)

Expense

It is the Department Administrator’s responsibility to monitor the Program Income PTA to ensure it is not significantly overspent or underspent. To do this, it is best practice to review expenditures to ensure they’ve been allocated appropriately between the main vs. Program Income PTA during monthly reviews and quarterly certifications. Expenses should be allocated to the Program Income PTA continually throughout the life of award to offset the income as much as practical.

E. What will happen to my Program Income PTA at closeout? Can I keep the left-over balance?

At closeout, the OSR closes both the main award and the Program Income PTA to ensure proper accounting. The department will move expenditures from the main award onto the Program Income PTA to fully expend those funds. Program Income is reported to the sponsor in a separate section on the Federal Financial Report (FFR) or through an annual report for NSF for each award.

Request this Chapter’s Archives

Request permission to view & download archived chapters from the Research Policy Handbook.

Request Access to Research Policy Handbook Archive