Categories of Sponsored Projects

Illustrates the major categories of sponsored projects, i.e., organized research (including both sponsored research and University research), sponsored instruction, and other sponsored activities.

Categories:

Recent Chapter Updates

-

Categories of Sponsored Projects

-

Categories of Sponsored Projects

-

Categories of Sponsored Projects

Questions about this policy?

Current Version: January 19, 2018

Original Version: July 1, 1994

Establishes procedures to meet the requirements of July 15, 1993 revisions to OMB Circular A-21, and the incorporation of the Uniform Guidance effective December 26, 2014 regarding the definition of University Research.

1. General Categories of Sponsored Projects

Sponsored projects at Stanford University are categorized under the following general headings:

- Organized Research, including Sponsored Research and University Research

- Sponsored Instruction

- Other Sponsored Activities

Classification of a sponsored project into one of these categories affects the calculation of Stanford’s Facilities & Administrative (F&A), i.e., indirect cost rates, and determines the appropriate rate to be charged. See Facilities & Administrative (Indirect Cost) and Fringe Benefit Rates: Definitions and Calculations, in the Research Policy Handbook.

Definitions and examples of these categories follow below.

2. Definitions

A. Organized Research

Research and scholarship activities include the rigorous inquiry, experiment or investigation to increase the scholarly understanding of the involved discipline. Organized research activities are funded by both external sponsors (Sponsored Research) and by Stanford University (University Research), and must be separately budgeted and accounted for. Together, these categories comprise the Organized Research distribution base, used to calculate the Organized Research Indirect (F&A) rate.

Any research activity that does not meet the criteria to be defined as Sponsored Research or University Research (Sections A.1 and A.2, below) must be classified as Departmental Research, and must be assigned to the Instruction and Departmental Research task service type in the accounting system. Examples of Departmental Research include: new faculty start-up funds which are provided on a non-competitive basis, funds from a faculty member's designated gift accounts expended for research that are not used to cover costs incurred on behalf of externally or University sponsored research, and University support of faculty salaries for non-sponsored research.

1. Sponsored Research (SR)

Research activities are properly classified as Sponsored Research if the research activity is sponsored (funded) by an external organization, i.e. a federal, state, or private organization or agency. The following are examples of sponsored research projects and, in all cases, these awards are made to Stanford University:

- awards for Stanford faculty to support their research activities

- external Faculty "Career Awards" to support the research efforts of the faculty

- external funding to maintain facilities or equipment and/or operation of a center or facility which will be used for research

- external support for the writing of books, when the purpose of the writing is to publish research results

- awards to departments, units or schools for the support of the research activities of Stanford University students or postdoctoral scholars, e.g., research training grants

1.a. Externally-funded Research Training Grants

Externally-funded research training grants are categorized as Sponsored Research (rather than Sponsored Instruction) where the primary activities of the trainees will be research.

The following characteristics indicate that a sponsored agreement should be treated as a research training grant:

- The primary purpose of the sponsored agreement is to provide research training to selected Stanford University students or postdoctoral scholars

- The award is made to Stanford University, with the provision that Stanford may name the trainees

- If a trainee leaves Stanford, the university may reassign the support to another qualified trainee

- Funding is normally provided to support the trainee, rather than to accomplish a specified statement of work or research project. Note that a research project may be described in a proposal for research training grant support, but the primary purpose of the award is to support the trainee.

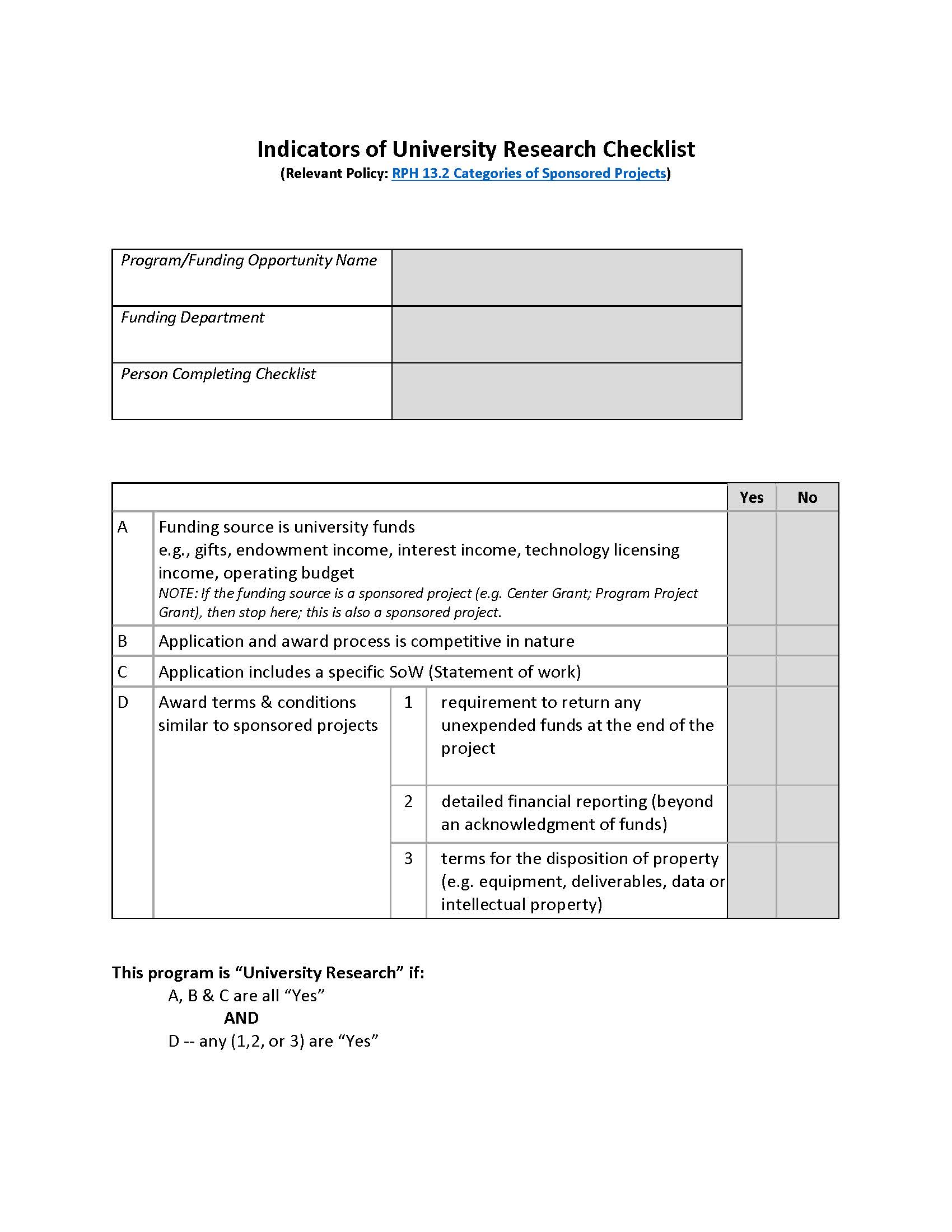

2. University Research (UR)

Research activity is properly classified as University Research if the activity is supported by either of the following (1 or 2):

- Funding that meets the following criteria:

a) derived from non-sponsored Stanford institutional funds, and

b) provided through a competitive application and award process, and

c) supported by statement of work or line of inquiry, and

d) providing assistance for a proposed activity which is characterized by the same factors which generally distinguish sponsored projects including:

- a requirement to return any unexpended funds at the end of the project or

- detailed financial reporting (beyond an acknowledgment of funds) or

- terms for the disposition of property (e.g. equipment, deliverables, data or intellectual property)

2. Cost Sharing (CS)

Cost sharing expenditures which are committed to be borne by Stanford rather than by the sponsor must be included in the OR base when the related sponsored activity is research. [See the section on committed cost sharing in RPH 15.3.]

B. Sponsored Instruction (SI)

Sponsored Instruction is defined as teaching and training activities funded by grants and contracts from federal or non-federal sponsors. Sponsored Instruction includes agreements which support curriculum development as well as teaching/training activities (other than research training) whether offered for credit toward a degree or certificate, on a non-credit basis, or through regular academic departments or by separate divisions, summer school, or external division.

Sponsored Instruction includes:

- curriculum development projects at any level, including projects which involve evaluation of curriculum or teaching methods; such evaluation may be considered "research" only when the preponderance of activity is data collection, evaluation, and reporting

- projects which involve Stanford students in community service activities for which the Stanford students are receiving academic credit

- general support for the writing of textbooks or reference books, video, or software to be used as instructional materials.

- Cost sharing expenditures which are committed to be borne by Stanford rather than by the sponsor must be included in the Sponsored Instruction base when the related sponsored activity is instruction. [See the section on committed cost sharing in RPH 15.3.]

C. Other Sponsored Activities (OSA)

Other Sponsored Activities (OSA) are defined as projects funded by sponsors that involve the performance of work other than Sponsored Instruction or Sponsored Research.

OSA may include:

- Travel grants

- Support for conferences or seminars

- Support for University public events such as "Lively Arts"

- Publications by Stanford University Press

- Support for students, staff, or teachers in elementary or secondary schools, or the general public, through outreach-related activities

- Projects that involve Stanford faculty, staff, or students in community service activities (where the Stanford students are not receiving academic credit for their involvement)

- Support for projects pertaining to library collections, acquisitions, bibliographies, or cataloging

- Programs to enhance institutional resources, including data center expansion, computer enhancements, etc.

- Cost sharing expenditures which are committed to be borne by Stanford rather than by the sponsor must be included in the Other Sponsored Activity base when the related sponsored activity is OSA. [See the section on committed cost sharing in RPH 15.3.]

3. Accounting

A. Accounting

Correct classification of funds is required. Errors in classification must be corrected upon discovery. Indirect (F&A) cost waivers or reductions will not be granted to remedy incorrect classifications of costs. See RPH 15.2, Indirect (F&A) Cost Waivers.

| CATEGORIES OF SPONSORED PROJECTS AND OTHER INSTITUTIONAL ACTIVITIES |

TASK SERVICE TYPE CODING (ACCOUNTING SYSTEM) |

FUNCTION CODE (SPACE INVENTORY SYSTEM) |

| Organized Research | No data | No data |

|

Sponsored Research (including Research Training Grants) |

SPONSORED_RESEARCH | R |

|

University Research (including Committed Cost Sharing and Overdrafts not removed prior to the project end date) |

UNIVERSITY_RESEARCH | R |

| Instruction | No data | No data |

|

Sponsored Instruction (including committed cost sharing for SI and excluding Research Training Grants) |

SPONSORED_INSTRUCTION | I |

|

Departmental Research (note: not a sponsored project , nor is it Organized Research) |

INSTRUCTION_AND_DEPT_RSCH | L |

|

Other Sponsored Activity (including committed cost sharing for OSA) |

OTHER_SPONSORED_ACTIVITY | I |

4. Indicators of University Research Checklist

Accessible version of the "Indicators of University Research Checklist" available as well.

Request this Chapter’s Archives

Request permission to view & download archived chapters from the Research Policy Handbook.

Request Access to Research Policy Handbook Archive