Cost Transfers

Categories:

Introduction

A cost transfer is an after-the-fact reallocation of costs associated with a transaction from one PTA to another. Cost transfers may also be called transfers of expense. Although costs should always be charged to the correct PTA, cost transfers are sometimes necessary.

Reasons for Cost Transfers

- to correct an error

- to transfer between tasks of the same sponsored project

- to remove disallowed costs

- to clear an overdraft at the end of a project

- Refunds and unexpected credits from the sponsor

Policy

Cost transfers must comply with the principles of allowable, allocatable, and reasonable. RPH 15.8 Cost Transfer Policy for Sponsored Projects addresses requirements related to cost transfers involving sponsored PTAs. These requirements are in addition to guidelines in Admin Guide 3.2.2, Cost Transfers. Cost transfers require careful monitoring for compliance with Stanford University policy, federal regulations and policies, and the federal cost principles that underlie all fiscal activities of sponsored projects.

Correction of Errors

Correction of errors is required on all PTAs no matter when they are found. Errors may include clerical errors (such as typographical errors or transposition of digits in the PTA and expenditure types). Other errors may be detected upon review or certification of monthly and quarterly expenditures. It may be that an employee's Labor Schedule was not updated, an individual's effort was redirected, or a purchase was charged to a PTA other than the one that ultimately benefited from the use of the items purchased. Cost transfers that represent corrections of errors should be completed within three months of when the error is discovered, and no later than six general ledger (GL) months after the original expense is posted to an award. Errors found during the required monthly expenditure statement review process should be corrected upon discovery.

Timing

- Cost transfers that represent corrections of errors should be completed within three months of when the error is discovered, and no later than six General Ledger (GL) months after the original expense is posted to an award.

- The best practice is to correct errors upon discovery during the monthly review. Errors found after the six GL months must be corrected and must be transferred to a non sponsored PTA.

RPH 15.8 Cost Transfer Policy for Sponsored Projects describes exceptions to the timeline

Systems to Transfer Costs

Cost transfers are submitted using the University's online Oracle Financials system iJournals and Labor Distribution modules.

- New iJournals are used to transfer all costs with the exception of salary or student aid

- Labor Distribution Adjustments are used to transfer salary expenses

- Allocation iJournals are used to distribute costs based on the proportional benefit to a project. Allocations are used when it is difficult to determine in advance how much to charge each PTA for a shared supply or service. Allocations are often used to distribute costs from Service Centers, Auxiliaries, or expenditure allocation PTAs. Often allocations are repetitive or are required on a repetitive basis

- Veterinary Service Center Cost Transfer Journal

Documentation

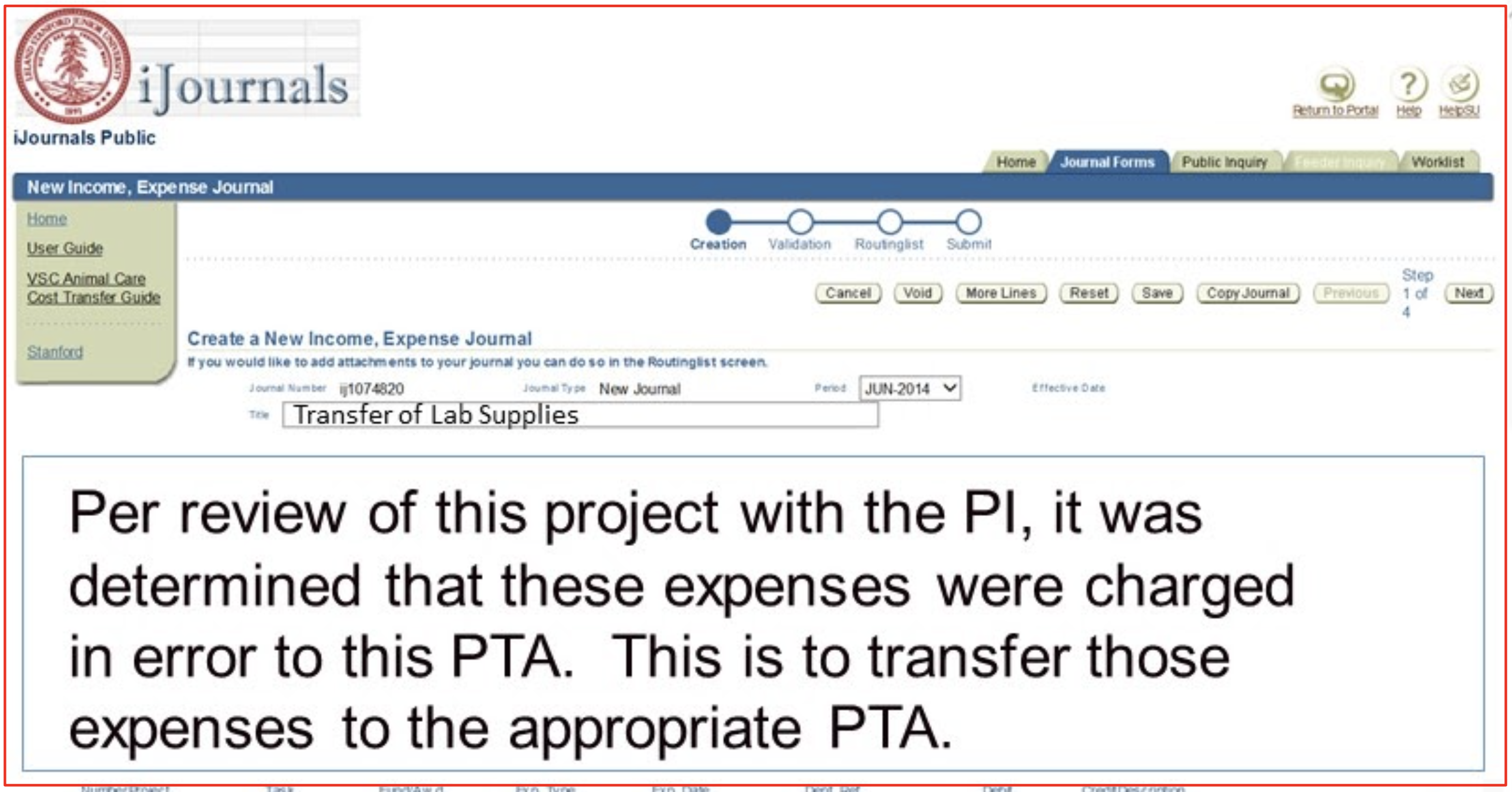

- All cost transfers must be supported by documentation that fully explains the error. An explanation merely stating that the transfer was made "to correct an error" or "to transfer to the correct project" is not sufficient.

- The cost transfer documentation for a sponsored project should be reviewed by the PI.

- The cost transfer procedure requires thorough documentation to support the transaction.

Created: 03.12.2021

Updated: 04.24.2024