Cost Principles

Categories:

Introduction

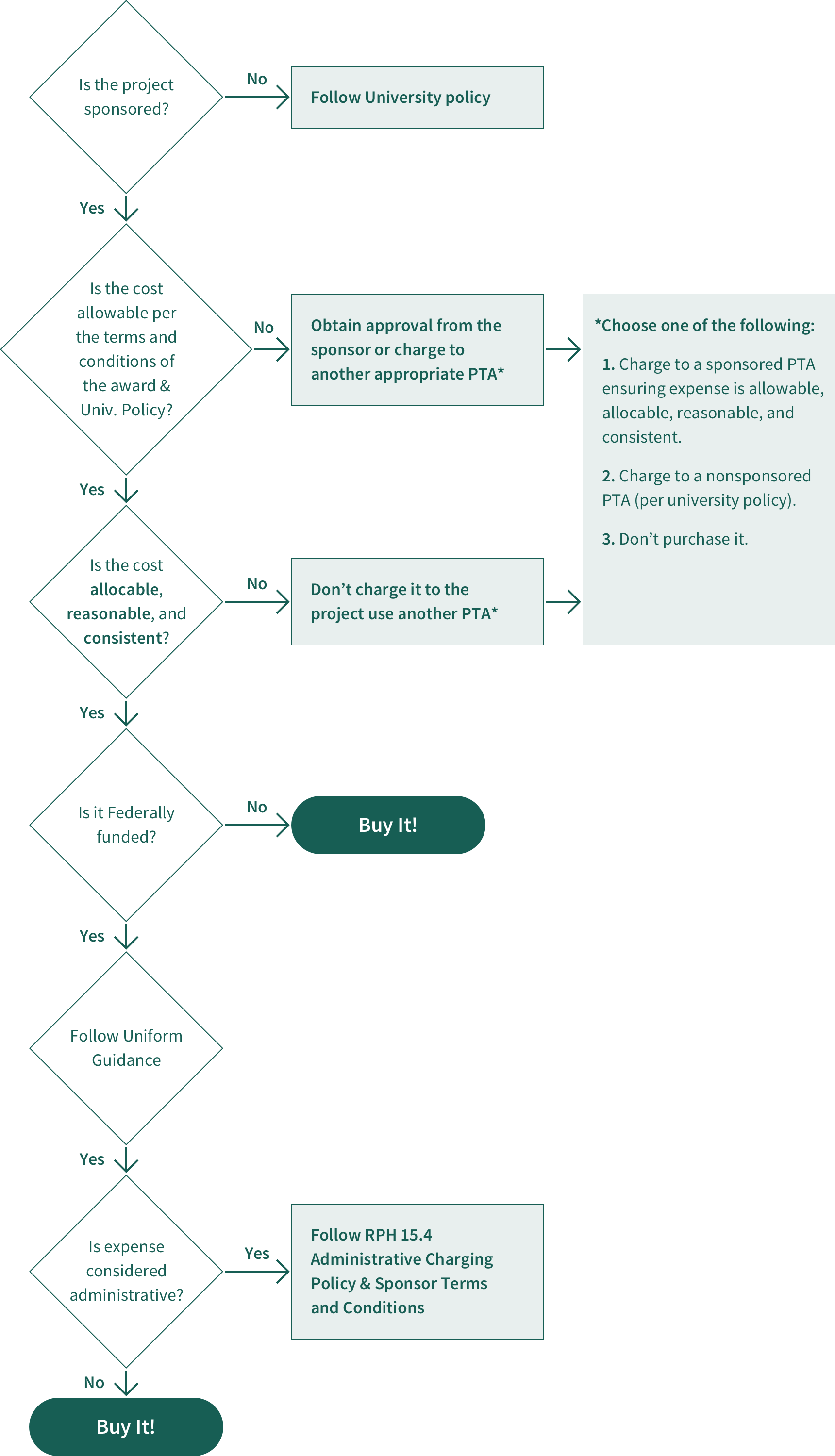

According to Stanford policy and federal regulations, an expense qualifies as a direct cost for a sponsored project when it meets all four cost principles. These principles govern costs that may be charged to federally sponsored projects either directly or indirectly.

Stanford generally applies these cost principles to the expenditure of non federal funds as well, however, in some cases non federal sponsors define allowable/unallowable costs differently than federal sponsors.

Any cost charged to a sponsored project must satisfy the following criteria.

-

The cost must be allowable as defined by federal regulations and/or by the terms of your particular award

-

The cost must be allocable, that is, goods or services involved are chargeable or assignable in accordance with the relative benefits received by the project(s).

-

The cost must be reasonable, that is, the cost reflects what a prudent person might pay.

-

Costs must be handled consistently across the university by following Stanford policy.

Allowable and Unallowable Costs

Costs are defined as allowable or unallowable for reimbursement by the government. A cost is allowable when:

-

It is not prohibited by University policy, Sponsor policy or Federal regulations

-

It serves a University business purpose, such as instruction, research, or public service

-

It is identified and coded correctly according to Stanford policy and federal regulations (regardless of whether or not it's a sponsored project)

-

It is incurred on a sponsored project according to the terms & conditions and the Federal regulation

Stanford Policy

Prior to paying ANY cost, you must assure that it is allowed by Stanford University policy which does not allow reimbursement to individuals for costs incurred for:

-

Personal amusement, social activities, or entertainment (outside of activities directly related to University functions or purposes, including employee-employer relations, performance improvement, etc.)

-

Stanford Faculty Club dues for individual members

-

Personal, social, or travel club dues

-

University parking permits for employees or students

-

Traffic citations for either personal or University vehicles

-

Personal services or personal purchases

-

Interest charges incurred by individuals for late payment of their own personal bills

-

Or any costs specifically disallowed by school or department policy

Federal Regulations

Once you determine a cost is allowable according to Stanford policy, you must determine whether it is allowable for reimbursement according to federal regulations. Costs are defined as allowable or unallowable for reimbursement by the government in the Uniform Guidance. The federal government asserts that federal funds may not be used to pay unallowable expenses. Unallowable expenses may NOT be charged either directly or indirectly to the federal government.

All costs at Stanford, regardless of funding source, must be coded as "allowable" or "unallowable" so they can be included or excluded from the indirect cost calculation as appropriate.

Expenses that are unallowable for federal reimbursement may be reasonable and necessary business expenses permitted by the University. Departments may incur these expenses but they must code them as unallowable.

The federal government will not reimburse certain items of cost as well as expenses supporting specific activities.

List of Federal Unallowable Items of Cost

-

Advertising (only certain types are allowable)

-

Alcoholic beverages

-

Entertainment

-

Fundraising or Lobbying costs (see Fundraising Flowchart)

-

Fines and penalties

-

Memorabilia or promotional materials

-

Moving costs if employee resigns within 12 months

-

Certain recruitment costs, e.g., color advertising

-

Certain travel costs, e.g., first-class travel

-

Cash donations to other parties, such as donations to other universities (small contributions for purposes of Employee Morale, e.g., a donation in lieu of flowers at a memorial must be coded as Employee Moral)

-

Costs in excess of University severance policy

-

Interest payments, except certain interest specifically coded as paid to outside parties and authorized by Financial Management Services (FMS)

-

Memberships in civic, community or social organizations, or dining or country clubs (seldom reimbursable by Stanford)

-

Goods or services for the personal use of employees, including automobiles

-

Insurance against defects in Stanford's materials or workmanship

-

In addition, Stanford University voluntarily treats the travel and subsistence expenses of University trustees as unallowable.

List of Unallowable Federal Activities

-

Fund raising (requires a unique task *)

-

Lobbying (requires a unique task *)

-

Commencement and convocation (can be allowable when charged to a Task with the appropriate Student Services - Service Type)

-

General public relations and alumni activities

-

Certain student activities, e.g., intramural activities, students clubs, etc.

-

Managing investments solely to enhance income

-

Prosecuting claims against the Federal Government

-

Defending or prosecuting certain criminal, civil or administrative proceedings

-

Housing and personal living expenses of University Officers

*Selling or marketing of goods or services (does not apply to selling goods or services internal to the university by its Service Centers)*For incidental fundraising/lobbying costs, charges may be made to the appropriate fundraising or lobbying ET.

It is crucial to code and categorize expenses correctly to comply with Stanford’s obligation to the federal government for both direct and indirect cost recovery. Our ability to obtain federal grants and contracts is dependent upon our performance in meeting federal requirements.

Unallowable Costs Can Be:

| Unallowable by Stanford | Allowable by Stanford and Unallowable for reimbursement by Federal Government |

Unallowable by Sponsor |

|---|---|---|

|

University expenses that are:

|

University expenses that are:

|

University expenses that |

|

These expenses will not be paid for by Stanford. If incurred, they must be paid for bythe individual. |

These expenses:

List of expenses unallowable for |

These expenses will not be paid for by the sponsor. Stanford may pay for the expenses, code as appropriate.

|

Use the Oracle Expenditure Codes and Descriptions to find the appropriate code for an expense.

Example of a cost that is unallowable for reimbursement by Stanford:

A Senior Research Associate purchases a leather briefcase and would like to use university funds to pay for the item. The designer briefcase is made of fine grain leather with brass trim and costs $1,250.

Explanation: The cost is not reasonable, it is not necessary for the performance of the person's job and is not permitted by University policy because it is a personal item. It does not meet all four criteria of Allowable, Allocable, Reasonable and Consistent so it must be paid for by the individual.

Example of a cost unallowable for reimbursement by the federal government, but allowable for reimbursement by Stanford:

An important faculty member is retiring from 35 years of service to Stanford. A party is given in his honor.

Explanation: Although this is something the federal government should not pay for as a direct or indirect cost, it certainly is an appropriate Institutional expense. This event should use the expenditure types: 52310 ALCOHOL BEV UNALW for all alcohol, and 52240 EMP MORALE for the food cost. The expenditure types designated unallowable for reimbursement by the Federal Government in both cases.

Example of a cost unallowable for reimbursement by the sponsor, but allowable for reimbursement by Stanford:

Example: A sponsor specifies that international travel costs cannot be charged to a particular project. Those costs may NOT be charged to that project, even though Stanford and federal regulation may allow them.

In addition, Stanford does not allow reimbursement for the following. These expenses will not be paid for by Stanford. If incurred, they must be paid for by the individual.

-

Personal amusement, social activities, or entertainment (outside of activities directly related to University functions or purposes, including employee-employer relations, performance improvement, etc.)

-

Stanford Faculty Club dues for individual members

-

Personal, social, or travel club dues

-

Stanford parking permits for employees or students

-

Traffic citations for either personal or Stanford vehicles

-

Personal services or personal purchases

-

Interest charges incurred by individuals for late payment of their own personal bills

-

Or any costs specifically disallowed by school or department policy

Allocable

Allocation of expense is the process of assigning a cost or a group of costs, to one or more PTAs in accordance with the benefits received. You should not allocate costs after the fact.

For example, a conference is held in Seattle that focuses on the "El Niño" effect on global climate. Jane, a postdoc working on a related sponsored project, will present her paper and interact with colleagues from other academic institutions. The trip will benefit the project, and the travel costs are therefore allocable to the project. Individuals directly involved with a project, particularly the PI, determine whether a cost is allocable to that project. In a case like this, when Jane’s department submits expense reports for reimbursement, the package should include the conference agenda or other documentation to support the relationship between the travel and the project which paid for it.

Reasonable

A cost is reasonable if a prudent person would purchase the item at that price under the circumstances prevailing when the decision to incur the cost was made. Determine whether a cost is reasonable by considering whether:

-

The cost is necessary for the performance of the activity

-

Incurrence of the cost is consistent with established institutional policies and practices

Jane was feeling rather good after her presentation and decided to celebrate in a BIG way. She brings back receipts showing that the cost of her final dinner in Seattle, exclusive of the wine, was $147 per person. Even though the trip was allowable and allocable, that cost is not reasonable. The cost principle of reasonableness stipulates that costs will be reimbursed only if a prudent person would have paid this amount. If not, the expense may not be charged to the project.

Jane is not eligible for full reimbursement of this expense from Stanford either, although she can be reimbursed for a lesser, reasonable amount.

Questions as to whether a particular expense is reasonable or not may be referred to a cognizant Dean's Office staff member.

Consistent

A cost is consistent when like expenses are treated the same manner under like circumstances. You can assure that you treat costs consistently by following Stanford policy.

How does an organization as complex as Stanford assure that expenses are being charged consistently? The answer lies in the translation of Government regulations into University policy, communicated throughout the organization and supported by necessary training and informational resources. Consistency is achieved when everyone follows University policy.

Created: 03.11.2021

Updated: 04.24.2024